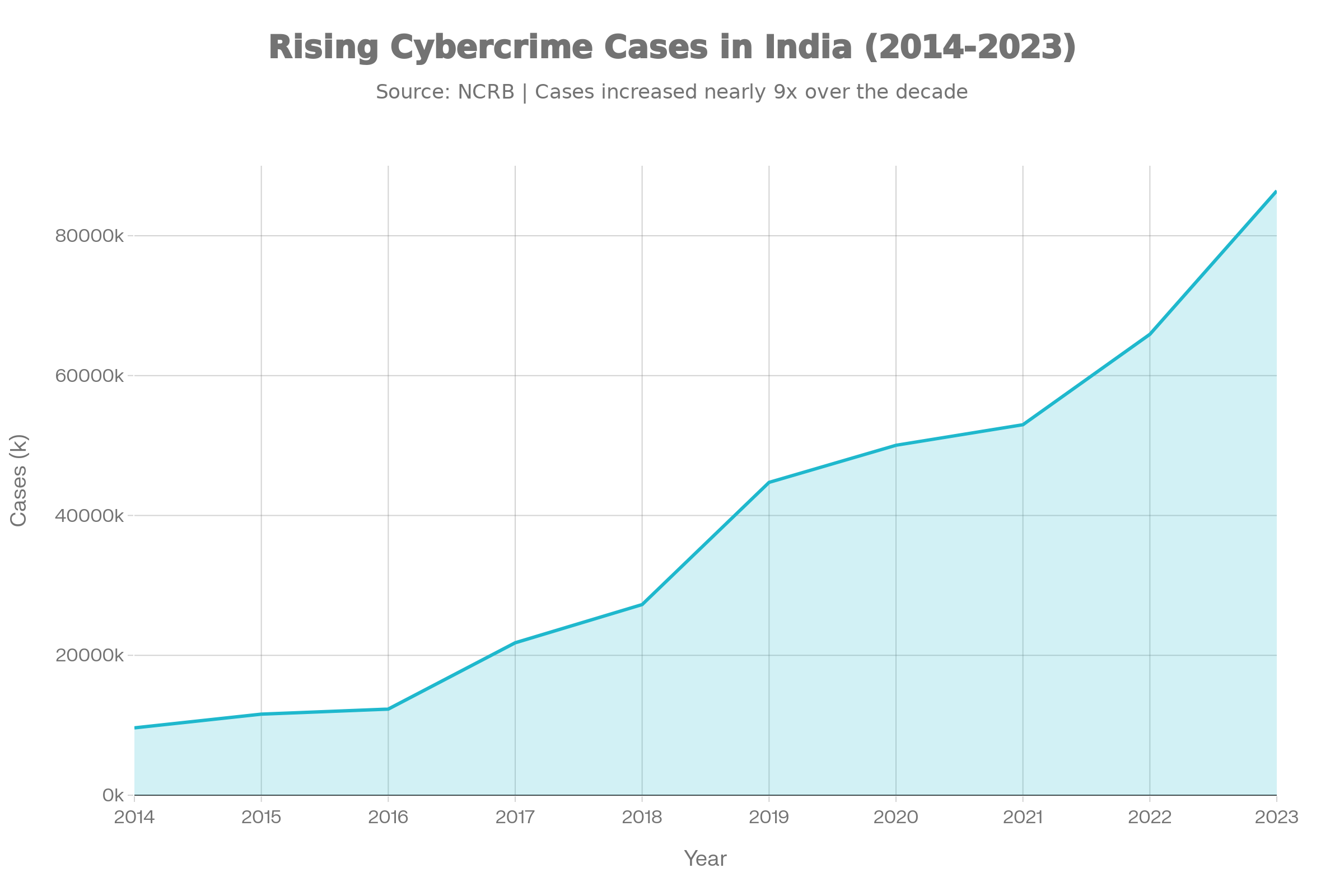

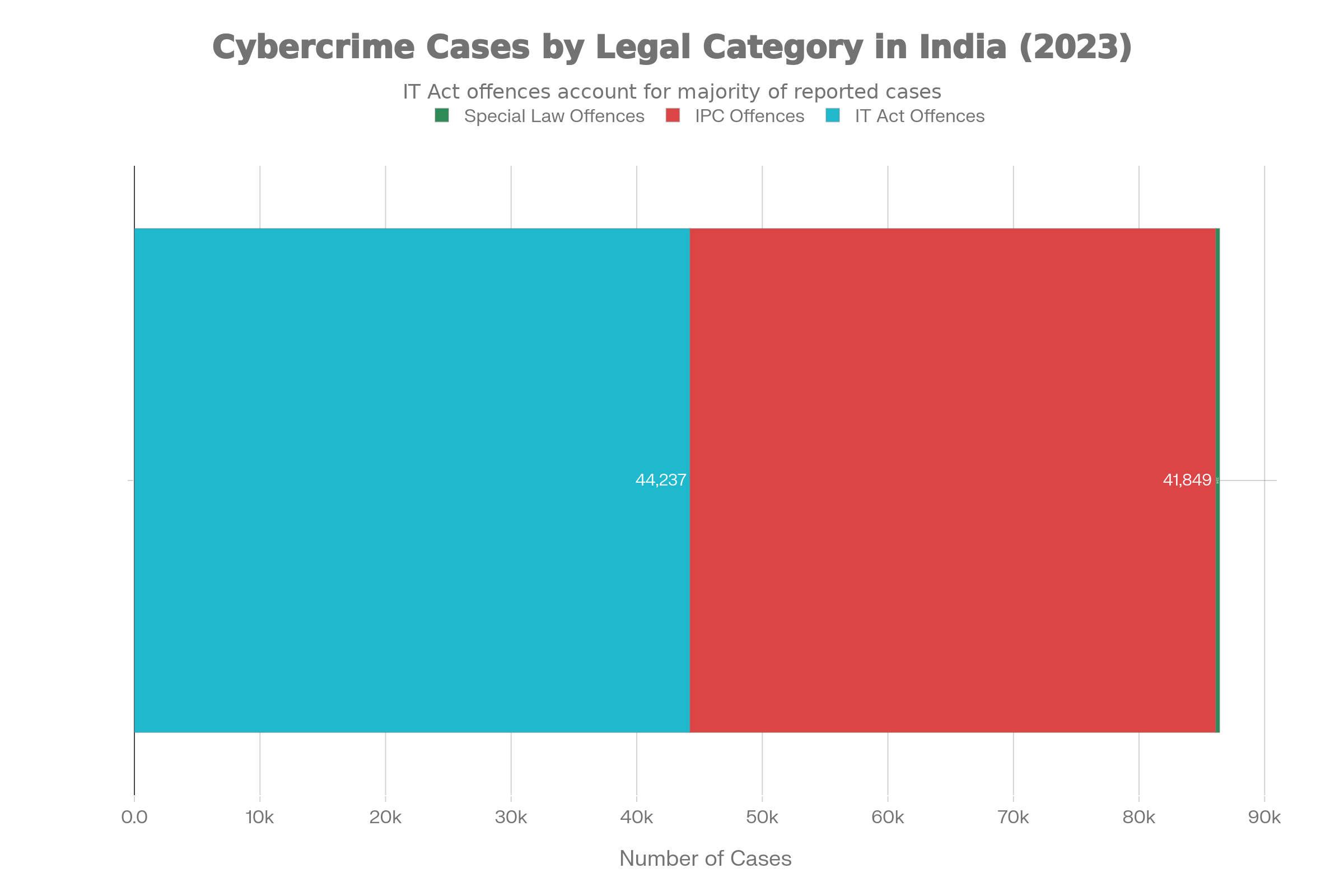

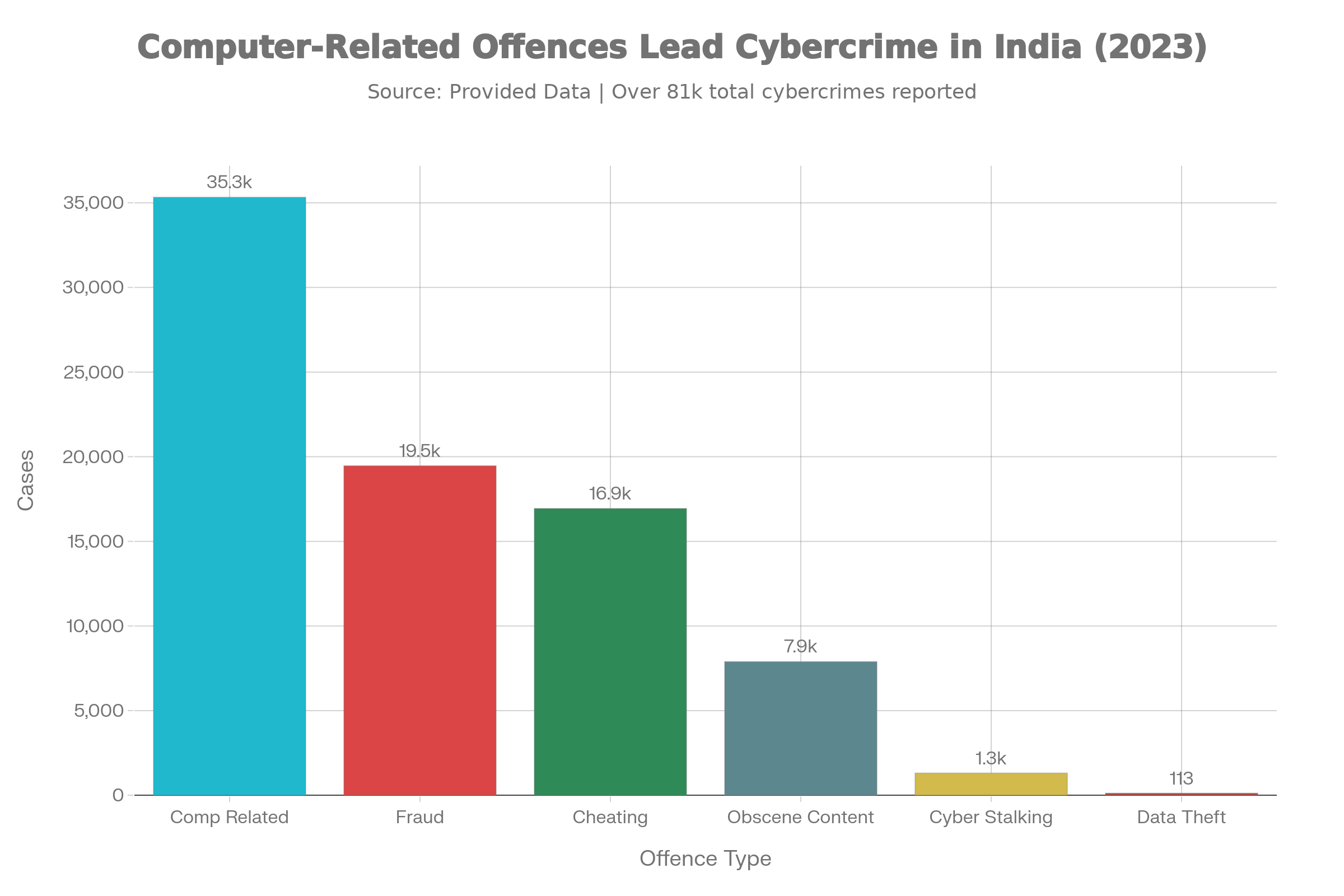

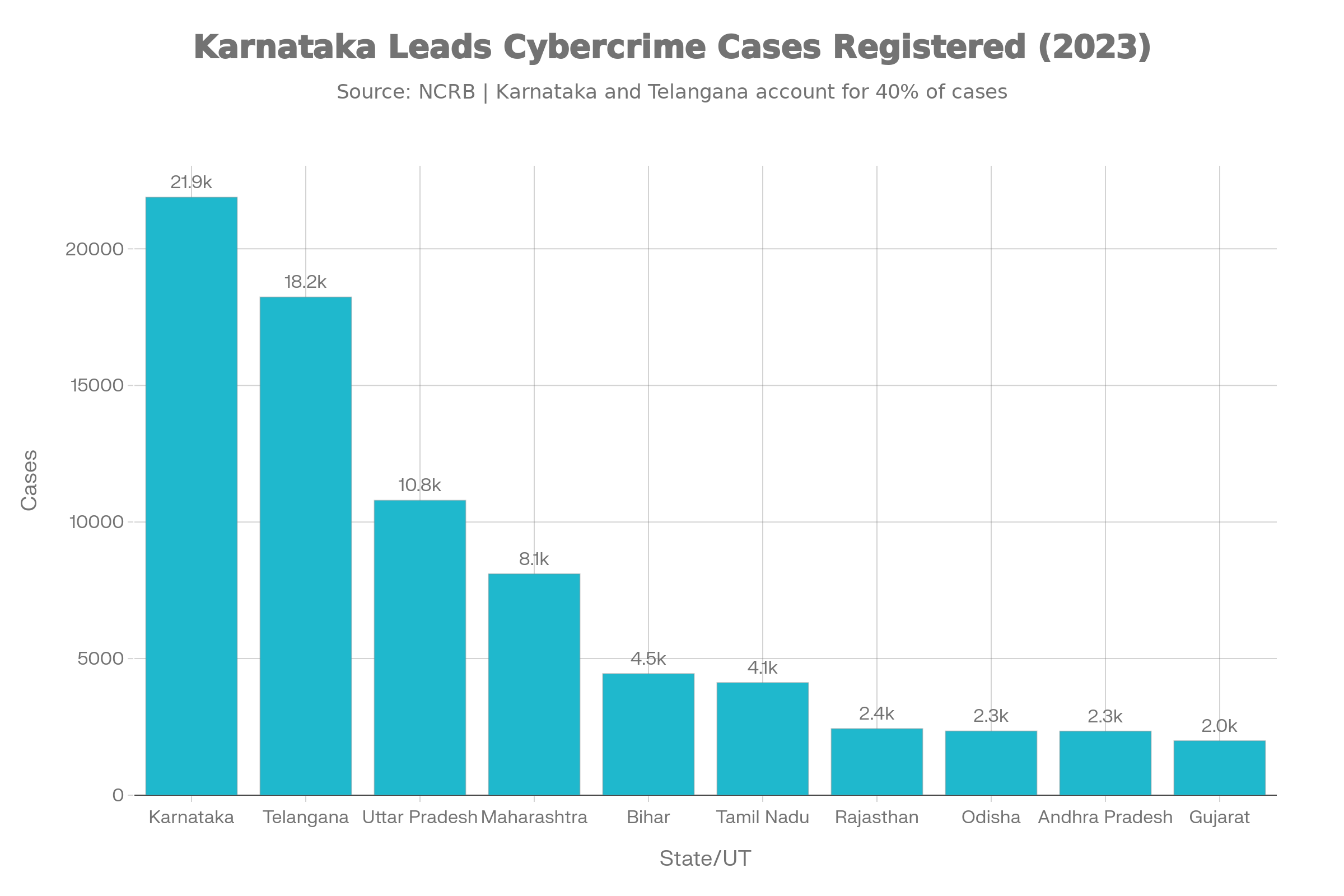

- Lately, cybercrime has taken a turn for the more sophisticated, with criminals cleverly shifting stolen funds through various bank accounts to stay under the radar.

- In response to this growing issue, banks are stepping up with an innovative solution: they’re looking to connect their systems with the National Cybercrime Reporting Portal (NCRP), overseen by the Ministry of Home Affairs.

- This integration could truly change the game for how banks tackle fraud and safeguard their customers.

- The Reserve Bank of India (RBI) has made it crystal clear in its latest advisory to all banks in India regarding the integration with the NCRP for handling complaints in real-time.

- Banks that haven’t yet completed the onboarding process are urged to do so “without further delay” and to prioritize this as “the highest priority.” The advisory also instructs all banks, even those already linked to the portal, to finalize API-based integration for immediate action on complaints.

Lately, cybercrime has taken a turn for the more sophisticated, with criminals cleverly shifting stolen funds through various bank accounts to stay under the radar. In response to this growing issue, banks are stepping up with an innovative solution: they’re looking to connect their systems with the National Cybercrime Reporting Portal (NCRP), overseen by the Ministry of Home Affairs. This integration could truly change the game for how banks tackle fraud and safeguard their customers.

The Reserve Bank of India (RBI) has made it crystal clear in its latest advisory to all banks in India regarding the integration with the NCRP for handling complaints in real-time. Banks that haven’t yet completed the onboarding process are urged to do so “without further delay” and to prioritize this as “the highest priority.”

The advisory also instructs all banks, even those already linked to the portal, to finalize API-based integration for immediate action on complaints. This integration needs to encompass all systems and delivery channels, with performance reviews happening regularly.

The takeaway is straightforward: manual processing just doesn’t cut it anymore. A real-time response is now the standard we should expect.

The Challenge

Cybercriminals are quick to transfer funds to obscure stolen money, making it incredibly tough for banks and law enforcement to recover those funds before they’re withdrawn or spent. Traditional methods of freezing accounts involve lengthy manual processes and back-and-forth communication between banks and authorities, which can really slow down response times.

India’s instant payment infrastructure is a remarkable feat, but speed has its downsides. When fraud occurs, money can zip through multiple banks, mule accounts, and exit channels in as little as 30 minutes.

Yet, many banks still handle NCRP complaints through manual workflows. This approach made sense when transaction volumes were lower. However, as digital transactions surge and fraud tactics evolve, the gap between the speed of money movement and the speed at which banks can respond is only getting wider.

The focus now is on bridging that gap. When a complaint comes into NCRP, we need to act fast: mark the lien, trigger the freeze, and kick off the investigation. This is what we call the Golden Hour standard.

Cybercriminals are getting clever with their tactics, using quick fund transfers to obscure stolen money. This makes it incredibly tough for banks and law enforcement to track down and recover those funds before they vanish. Traditional methods for freezing accounts can be a real slog, involving lengthy manual processes and back-and-forth communication between banks and authorities, which can really slow down response times.

India’s instant payment system is a fantastic achievement, but that speed can be a double-edged sword. When fraud happens, money can zip through various banks, mule accounts, and exit channels in as little as 30 minutes.

Yet, most banks still handle NCRP complaints through manual workflows. That approach worked when transaction volumes were lower, but as digital transactions surge and fraud tactics evolve, the gap between the speed of money movement and the banks’ response time is growing wider.

The aim now is to bridge that gap. When a complaint comes in through NCRP, the response needs to be swift: mark a lien, trigger a freeze, and kick off an investigation. This is what we call the Golden Hour standard.

The Proposed Solution

Integrating APIs with the NCRP presents a game-changing strategy for tackling fraud. Here’s a breakdown of how it all works:

Central Repository for Fraud Data

Banks will send fraud-related information to a central repository overseen by the NCRP. This centralized system will serve as a comprehensive database, gathering fraud data from all participating banks. By bringing everything together in one location, the NCRP will offer a clear and unified perspective on fraud cases throughout the banking industry.

Automated Account Freezing

As soon as a fraudulent transaction is identified, the API integration will enable banks to automatically update the central repository with the necessary details. This smooth communication will allow for the immediate freezing of affected accounts, eliminating the need for any manual processes.

Daily or Weekly Synchronization

When it comes to Daily or Weekly Synchronization, banks will keep their own databases in sync with a central repository, either daily or weekly. This routine update guarantees that every bank has the most up-to-date fraud information, allowing them to act swiftly to curb any further fraudulent activities.

Enhanced Blacklisting and Tracking

In terms of Enhanced Blacklisting and Tracking, having real-time access to detailed fraud data means banks can quickly add known fraudsters to their blacklist. This feature enables them to identify and block transactions involving these individuals much faster, significantly lowering the risk of stolen funds being misused.

Standard Operating Procedures (SOPs)

As for Standard Operating Procedures (SOPs), the Indian Cybercrime Coordination Centre (I4C) will set up SOPs to help banks manage fraud cases effectively. These procedures will outline steps for freezing and unfreezing accounts, as well as handling negative KYC details to stop fraudulent account openings. By implementing these SOPs, the industry can ensure a consistent and efficient approach to tackling fraud.

Benefits of the Integration

Faster Fraud Response: By automating the account freezing process and centralizing fraud data, we can drastically cut down the time it takes to tackle cybercrimes.

Improved Coordination: A central repository will boost data sharing among banks, leading to better teamwork and more effective fraud prevention strategies.

Efficient Record-Keeping: Regularly syncing fraud data will enable banks to keep their records accurate and up-to-date, enhancing overall operational efficiency.

The proposed API integration with NCRP represents a major leap forward in the battle against cybercrime. By harnessing the power of automation and centralization, this solution will empower banks to better protect their customers, recover stolen funds, and ultimately strengthen the security of the financial system.